Article also available in <link _top>

Wang MingJun

Foundry Supplies Committee of China Foundry Association (Director), Dalian Foundry Association (Chairman), Dalian Xinlong Casting Industry Co., Ltd (President)

Summary

Refer to the current economic development and the market supply-demand relationship under the domestic and international circumstance, in the article we analyze and forecast the price tendency of the material, and discuss the development of China foundry industry. Our purpose is through grasp the market, adjust the production structure promptly and reduce material costs to take the initiative respond to the market changes and create more direct economic benefits.

Preface

The consumption of foundry industry in energy and mineral resources are not only variety but also a huge number. According to statistics, in china there are over 30 million tons of castings were produced in 2007, which need 37.5 million tons of metal, 33 million tons of molding materials, 10.8 million tons of various refractory, and other kinds of auxiliary materials 11.25 million tons, in total, all the foundry materials come to 92.55 million tons. At present, in China the contradictions between economic development and energy resources become more and more outstanding, so it is necessary to establish a resource-saving and conservation awareness, choose high-quality casting materials, reduce material consumption, and establish a conservation-oriented society to the industry. In recent years the world economy maintain a rapid growth. Meanwhile, the economy in developed and developing countries also change rapidly, and the regional structure of the world economy changed, many problems and contradictions became more and more obviously, especially the global economic imbalances, the increasingly tense relationship of the international market, economy risk increased, and uncertain factors increased. The economic growth is the driving force for the social development. Under the circumstance of high-speed economic growth and social reformation, china is experiencing a series of social problems and the idea vicissitude. There is also a great impact to the material prices. In order to raise the economic benefits of the enterprises, the quality and the prices of the materials seem to be particularly important.

The development and influence of the international economy

Chinese economy keep rapidly develop to promote world economy growth. It was make the biggest contribution to the world economy growth in 2007. However, the current international economy environment has also formed the larger challenges and pressures for Chinese casting material price, the major factors as follows:

1) International petroleum and food price keeping the high fluctuation, which forms a big pressure on china imported inflation.

2) The pressure from RMB appreciation keeping greater which lead to the import inflation and imbalance trade problems become more and more serious. Meanwhile, the regulative effects of the monetary policy to the oversized credit and the investment become weaken.

3) The US, Britain and Canada are in a rate cut cycle, and the European Central Bank also pause raise the interest rates, while China is raising the interest rates. The market hold the anticipation of the continuous rate-raising and RMB appreciation, so the international investment capital will possibly form a large impact on China.

Under this world economy environment, the macro-control policies of china will be sustained in 2008. In view of the above varies of reasons, the materials price will be also very fluctuated, and expected to keeping growth.

Influence of the Macro-Control and Analysis of the Material Price

Non-Ferrous Metals:

1) Reviewing the price quotation of 2007 and forecasting the tendency of 2008

In 2007, China Non-ferrous metal industries are in the booming period. The market consumption growth rapidly, which benefited from the strong consumer support to Chinese rapid economic growth and owe to the related industrial policy to promote the trade integration. However, the non-ferrous metal market of China is accelerated driven to concentration and integration by the non-renewable and scarce metal resource.

We believe that the non-ferrous metal supply and demand will more tense flexibility in 2008. To combine the low inventory condition and the resources commodity obtains the investment approval gradually, we may forecast that the booming factor of the non-ferrous metal industry has not extinguished.

2) Analyze Part of the Material Price

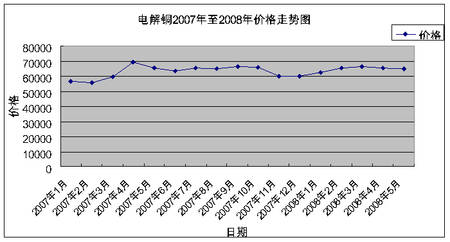

2.1) Electrolytic Copper

Copper industry is the key industry in the national economy. At present there are 124 industries in China, 113 of them are use for the copper products, taking some 91%. There is also a wide connection between copper-processing industries and other industries. Last year, copper consumption in China is estimated to account for a quarter of global copper consumption and increase significantly. The copper price, in recent years, is affected by many constraint factors in China. And in the long-term, prices for the performance of China's and India's economy growth as the representative of consumer demand, and confront with the production supply of the representative rich natural resources and exploitation of copper smelting technology progress. As both supply and demand prospects are very good, the copper price has no long term fundamentals support as petroleum price. At the same time, the balance relations between demand and supply have the time lag. There are many links form the macroscopic supply and demand transforms to the terminal.

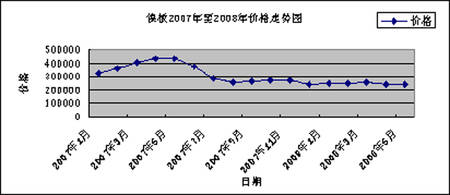

Graph 1 shows the price of Electrolytic Copper during January 2007 to May 2008, the highest price is RMB 69,380 per ton in April 2007, and the lowest price is RMB 55,590 per ton in February 2007, with a margin of RMB 13,790 per ton. Although there is a slight increase in the first three months in 2008 than that of 2007, the price is generally stable. Consequently, the price tendency in 2008 we assume is steady rising, the price won’t be large fluctuation besides the special circumstance and manipulation.

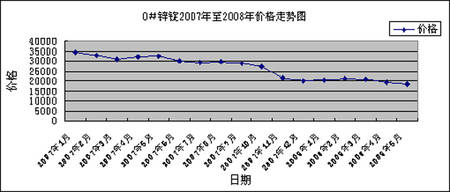

2.2) Zinc Ingot

The production of refined zinc has experienced a steady increase in China in 2007, with some 3.3395 million tons during the first 11 months, an 18.9% increase year on year. The zinc price generally went with the copper price, but a little bit lower.

Graph 2 shows the price of the zinc ingot in China during January 2007 to May 2008, from which we see the spot price experienced a months-long stable period around RMB 30,000 per ton with slight fluctuations in the first half year of 2007, and then a year-long continual drop after the last rise in London in May during the rest months because of the superfluous supply and the earthquake etc. Consequently, the price tendency in 2008 will continue to drop with slight fluctuations.

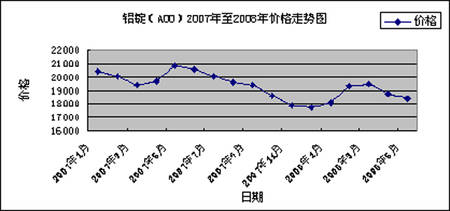

2.3) Aluminium Ingot

The international aluingot price in 2007 didn’t show much fluctuation on the whole except in short periods. The aluingot price in London kept between US$2,400-3,000 per ton with a slow rise to the upper limit of US$2,950 in the first half year, while in the later part of the year, influenced by the turbulence of the international money market caused by the subprime mortgage crisis, aluingot price, together with other motels in fact, has experienced another rearrangement and stayed around US$2,400, the floor level until the end of the year. Comparatively, aluingot price in domestic market stayed between RMB18, 000-20,000 most of the time with the largest fluctuation around RMB3,000. However, the prompt goods kept a larger fluctuation than futures and the price of Changjiang Nonferrous99.7 has scattered between RMB17,500-21,5000 for the whole year.

Graph 3 shows the aluingot price during the same period, in which it started to drop slowly in the first season in 2007 and kept dropping after a single rise in the second season until the end of the year. As the supply has kept a surplus in 2007, the price tendency in 2008 will continue to drop with slight fluctuations.

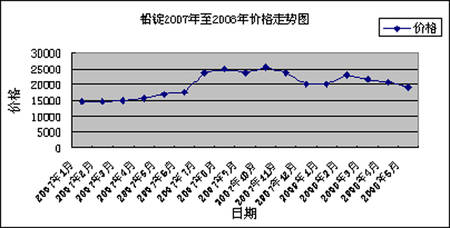

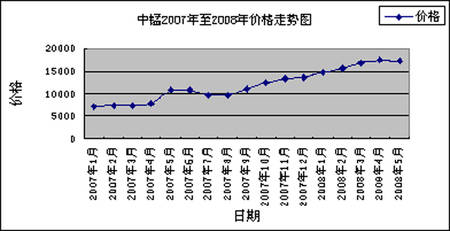

2.4) Lead Ingot

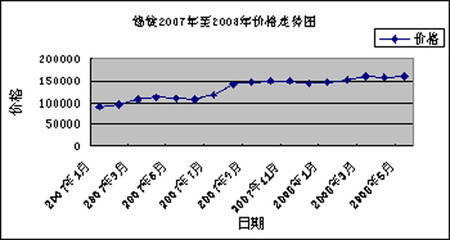

According to the International Lead and Zinc Organization, the overall short supply of lead is 63,000 tons in 2006, and it turns to 136,000 tons in 2007, while the refined lead increased 1.1% compared with the same period of 2006 in 2007. However, the situation will be changed with the export of the Ivernia’s Mine Magellan in 2008, with boasts 3.5% of the total lead output.

In domestic market, to avoid the over enlargement of the rough lead industry, the over pollution and excessive energy consumption, the national Financial Department has improved the tariff of the refined lead from 10% to 15%.

Graph 4 : The price has kept rising in 2007, exceeding RMB20,000 in July and to RMB24,860 in August. There shows a little fall from the first season in 2008 to now. So the price tendency of lead in 2008 will has the rise place.

2.5) Nickel Plate

The overall output of nickel is 1.48 million tons in 2007 over the 1.36 million tons in 2006; the consumption is 1.41million tons over the 1.39 million tons in 2006. Although the demand in China increased, the decrease in Europe has kept the nickel price in a low level and dropping after June 2007 .We think the price will be mainly influenced by the supply changes in 2008, and we are confidently expecting a further demand from the emerging economies like China. Take the China’s large stainless steel manufacturers for example. Taiyuan Iron&Steel Company Ltd (TISCO) plans a 3-million-ton output of stainless steel in 2008, compared to the 2-million tons in 2007. Baosteel Company Ltd (Baosteel) plans a 1.2-million-ton output in 2008, over 200,000 tons higher than 2007. Others like Zhangpu and Lianzhong also have a total planning output about 2 million tons in 2008. That is to say, the stainless steel production will face a vigorous growth in China, which surely will draw the demand for nickel back to an optimistic level.

I hold the negative view of the nickel price in 2008. There might be some obstacles against the price increase, but in a long-term, the high price of the Nickel is difficult to turn around. Considering the balance of the demand and supply, as well as the devaluation of U.S. dollar, the price tendency in 2008 will steady drop with slight fluctuations, the price won’t be large fluctuation besides the special circumstance.

2.6) Tin Ingot

Indonesia,as the largest tin producing country, it’s yearly capacity are 120,000-130,000 tons (the global total output are 350,000 tons), which influence the global price of the tin greatly. The gap between tin supply and demand is further widened in 2007, which come to 21,000 tons. As the statistics show, the solder account for 52% of the global tin consumption, which in Asia account for 80% and only China account for 55%. In 2007, because of the reorganization of the Indonesia government, some of the smelteries and small mines were closed, which caused a short supply of tin and an increase in price. The Indonesian government stated there is no intention to restrict tin export, but a further regulation of tin business on the island and the tin exporting management to avoid illegal exploitation.

However, Indonesia is expresses to control the output of tin and sustain the international price. At the beginning of 2008, the tin export decreased and the output increased slightly in both China and Indonesia, the international demand also kept stable, but china faced a vigorous increase. Therefore, in 2008, the tin price will steady rise with slight fluctuations.

Ferroalloy

1) Reviewing the price quotation of 2007 and forecasting the tendency of 2008

In order to adapt to the adjustment and promote the development of industrial structure, efforts to rectify the order in the industries with high energy consumption and develop working on energy conversation and pollutant discharging decreases, which through establishing industrial admittance condition, raising the electricity price, environmental protection request, eliminating the backwards, limiting the minimum yield and so on. Especially for the ferroalloy industry, washing out the backwards of production work started full swing. Our country continues to standardize it’s production of export, through raising customs duties, strengthening the export administration control, limiting the price in custom. In 2007, influenced by the national policy, there’s a wide price fluctuation in the ferroalloy market. The output and import amount had fallen off sharply that caused the price visibly increasing.

As the sustaining influence of national policy, the characteristics of the ferroalloy industry in 2008 as follows:

- Ferroalloy output will be continuously increased with the increase of

crude steel. The growth rate will be rise by the influence of the nation policy.

- Ferroalloy import continued to rising, especially for high-carbon ferrochrome and middle-low-carbon ferrochrome. With the rise of the stainless steel output, the demand of ferrochrome became larger, while the import price can’t meet with the domestic produce, of which led a sustaining rise to import amount.

- Ferroalloy export will be declined greatly, even face a negative growth. In 2008, ferroalloy tariff are general increase, as well as ferrosilicon and silicon-manganese are hindered by antidumping, all these that will cause a drop of export amount about the ferroalloy.

- The ferroalloy market is complicated and changeable, and competition is becoming increasingly acute. A series of factors (a continues increasing on the price of some import products, the steep rise on the prices of coal, electricity and coke) may further increase the cost of ferroalloy, as long as China begin to implement the tight monetary policy, reciprocal outstanding payment and the financial strain make many enterprises hard to continue their production and operation. Totally, the price will continue to move up.

2) Analyze Part of the Material Price

2.1) Ferrosilicon

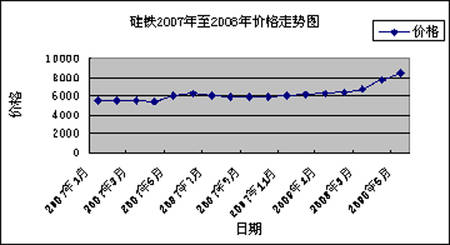

In early 2007, domestic market sales remained stable, 5500 RMB per ton. In February, as the strain on highway and railway, the transport costs increased, which caused a rise on price by small margin. In April, the price slowly setback, especially in Nei Meng district, the price declined to 5460 RMB per ton. During May, because the running of the electricity price, ferrosilicon once jump to 6320 RMB per ton at peak. From the 1st,June, the rates of tariff raised to 15%, which strongly influenced the export. Some resources which for exporting sold to the domestic market became oversupply, of what bring a fall.

Graph 7: The market still run in high price. Though Europe adopted measures on the antidumping, European price had raised to 1400 USD per ton and the small- size domestic enterprise management was further enhanced, the ferrosilicon export to Japan and Korea maintained the amount. These made a balance between supply and demand by the influence of power and coal price, so the tendency in 2008 will continue to move up.

2.2) High-Carbon Ferromanganese and Medium-Carbon Ferromanganese

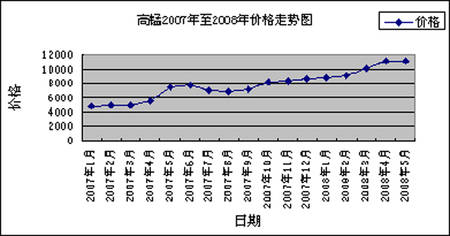

Since import manganese mineral kept a high price in 2007, the manganese market price strongly soared from March, as well as new policy about the electricity price, continuously rainless period in South, to stock up factitiously, from the graph 8 know: the high-carbon ferromanganese price reached a new historic height (8650 RMB per ton), while in Chart 9 medium-carbon ferromanganese reached 13450 RMB per ton at the peak. From December, the rumor about the ferroalloy tariff adjustment which was substantiated, led the domestic quotation continue to rise. For example, at the end of December, the quotation in domestic silicon-manganese market was once in a high level: the high-carbon ferromanganese (Mn65) quote 10000—12700 RMB per ton, while that of medium-carbon ferromanganese was 17000 RMB per ton. From 1st January, 2008, the tariff of some alloy such as ferromanganese increases to 20%, which will influence the domestic market. So we forecast the trend of high-carbon ferromanganese price will continue to move up, low-carbon ferromanganese price will continue to move up and there is little chance to fall in 2008.

2.3) High-Carbon Ferrochrome, Middle-Carbon Ferrochrome

In view of the overall situation, the trend of ferrochrome market was still downwards in 2007。Graph 10 and Graph 11: The price of high-carbon ferrochrome increased from 7380 RMB per ton (the lowest in 2007) to 17000 RMB per ton at the peak in the first quarter of 2008. The price of low-carbon ferrochrome increased from 11150 RMB per ton (the lowest in 2007) to 24500 RMB per ton at the peak in the first quarter of 2008.

From 1st, Jan, 2008, the government declined the import tariff rate, as long as the price showed significant advances, the electric power crisis in South Africa and the accident about ferroalloy factory, which all put the price of ferrochrome reached new historic height in the European and American market. The price in foreign market is higher than Chinese, which bring on the lack of production and the high price in domestic market. So we estimated the price of high-carbon ferrochrome and the low-carbon ferrochrome will both continue to move up.

Pig Iron Series: Reviewing the price quotation of 2007 and forecasting the tendency of 2008.

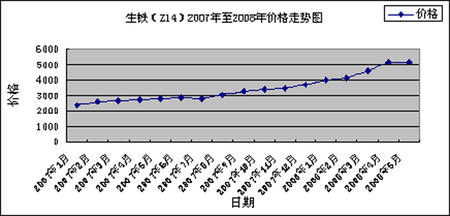

From the graph know: in Jan, 2007, the price is RMB 2,350 per ton, in Dec, 2007,the price is RMB3,694 per ton, which up by 57%. On 31th, May, 2008, the price had came to RMB5000 per ton or so. From the Jan,2008 to now, the price have up by 35%. Compare to Jan,2007, it have up by 113%.

From the graph know: in Jan, 2007, the price is RMB 2,350 per ton, in Dec, 2007,the price is RMB3,694 per ton, which up by 57%. On 31th, May, 2008, the price had came to RMB5000 per ton or so. From the Jan,2008 to now, the price have up by 35%. Compare to Jan,2007, it have up by 113%.

The price of the ore which are imported from Brazil/Australia and the coke all keep raising. Meanwhile, in order to welcome the Olympic Games and reduce the pollution, more than one thousand of small smelting works have been closed in domestic. So the estimated price of pig iron and scrap steel will both continue with a little rise.

Stainless Steel Series: Reviewing the price quotation of 2007 and forecasting the tendency of 2008.

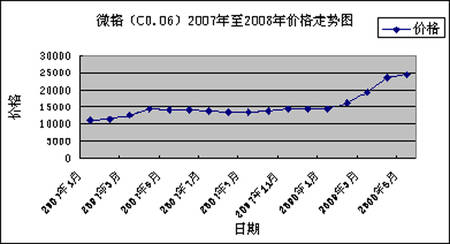

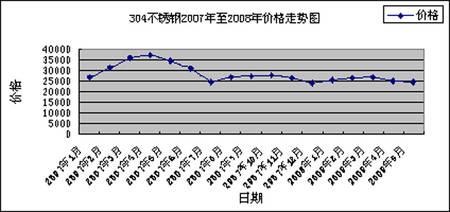

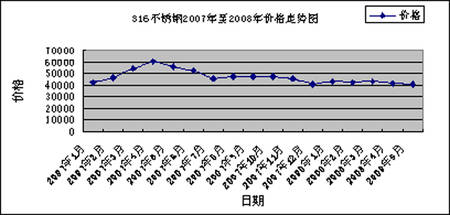

It is well know that nickel and chromium are the main raw materials of the stainless steel. The chromium price was steady in 2007 in the international market, so the nickel price can directly reflect the stainless steel markets. The nickel price experienced a drastic change in 2007. In May it was rise to the peak which broke the record, since then the nickel prices gradually come down. The stainless steel experienced a drastic change with the price change of the nickel too. From the graph 14 show the stainless steel 304 (exclude taxes): the prices between RMB27000-36000 per ton from Jan. to March, and up to RMB37,275 per ton from March to June, then dropped to RMB24,420 per ton. Stainless steel 316 (exclude taxes) prices are 4-5 million in the whole year and the highest price up to RMB52,500 per ton. So we estimate the price of stainless steel will be Stable and it would be rise while the chromium price rise.

Coke: Reviewing the price quotation of 2007 and forecasting the tendency of 2008.

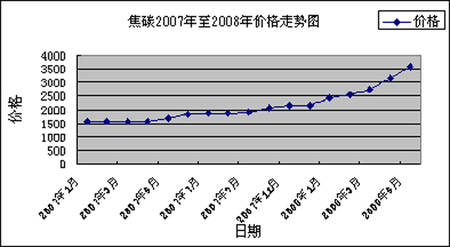

The graph 16 shows: the coke price rise from RMB1570 per ton to RMB2150 per ton in 2007, which up by 37%. In May,2008, the price is RMB3700 per ton, which up by 72%.

At the beginning of 2008, because of the rainstorm, Queensland , which was the biggest country export coal and coke had to reduced the volume of exports. In domestic, the coke resource shortage and the mining accident make the price raise greatly. From 1st,Jan,2008, the Ministry of Finance has adjust the export duty from 15% to 25%. Moreover, in order to welcome the Olympic Games, our country carry out several policies, which will add the produce cost. At present, most of coke enterprises increased the investment on environmental protection which will add the product cost in the short-term. So the estimated price of coke will continue to keep a little rise.

Ancillary Materials

1) From April,2007, the alumina sand, kaolin all keep rising, which have came to 40%, and will continue to keep the tendency.

2) The metallurgy magnesium sand which production place in Liaoning province all keep the rising tendency.

3) The price of chromium sand which production place in South Africa also go upward, from the first half of 2007, it have go up by 50%.

4) Because of the sufficient suppliers, the price of the zirconium English sand/powder keep falling.

Conclusion

Based on the current complex market price, we put forward the following proposals:

1) Do not fix the price of casting immediately in the daily production and business activities, we should set one order to one quote. If the purchaser requires to confirming the whole year’s price, the additional terms should be set in advance which allow to adjusting the casting prices along with the casting material prices fluctuation. So that it could reduce the losses of casting factory. At the same time, it is fair for both supplier and purchaser.

2) Adopt the used material as substitutes. Fox example: the scrap copper lines, used bright lines and cables should be substitute as the electrolytic copper in copper castings, which have better qualities and could save about RMB 1,000-2,000 per ton. The scrap aluminium also can be used in aluminium castings and it could save RMB 1,000-4,000 per ton. In particular for the production of stainless steel castings, adopt the 304,316,409,430 and second series of stainless steel scrap materials instead of the composite material of ferrochrome, nickel plate, molybdenum iron and pure iron, which could reduce the cost about RMB 1000-5000 per ton.

3) Use the new energy-saving materials, for instance, the ramming coke which has the characteristics with high density, large calorific capacity and long time combustion, it can save at least 10%--15% of the money。When produce the nickeliferous castings with requirement of low carbon content, use nickel alloy related material instead of nickel plate which can reduce the costs RMB1000-3000 per ton at least. The economical fund would be the direct profit of the factory. We recommend the manufacturers to adopt these proposals. The more proposals won’t be presented due to the limited time.

The fluctuation and potential inflation of financial market in 2008 will interfered in the future economy development, the price of the petroleum and the grain all rising, as well as the foreign exchange flow into the emerging markets. At the same time, domestic CPA rises continuously. The <<Country New Labor Law>> promulgated in March had stipulated the minimum wage level lead to the increase of the factory costs. The interest was rose by the Central Bank continuously lead to the capital market price move up. All these economy transmission enlarged the company costs gradually. As the casting material demand is related to the macro economic development positively, the growth of the demand speed will be impacted by the development of the future economy. From the current economic indicators, including the impact of domestic and international contradictions between supply and demand, the dollar exchange rate, the International Fund, the interaction between domestic and international prices, the world and the major country economical trends, the impact of domestic and foreign stocks which were lead to the unpredictable situation. Therefore the fluctuant macro-economic will affected the growth of future demand of metals should be considered.

Since the current stocks remain low, the value of the commodity obtains the investment approval gradually. We believe that in 2008 the supply and demand relationship is still tight, the booming factor of bull market hasn’t eliminated, and the foundation support of casting high price still exists.

The market is competitive and the price is unpredictable, please pay attention!